Time Series Analysis

A

time series is actually a sequence of data points recorded at regular intervals

of time (yearly, quarterly, monthly, daily). Time series includes two types:

- Univariate – involves a single variable

- Multivariate – involves two or more variables

Let

me present you a list of examples of time series:

- Monthly

or daily precipitation of a region - Daily

stock prices (opening, closing) over a period of years/days. - Monthly

bike sales over a period of 3 years - Annual

unemployment rate over a period of 10 years

Forecasting the Time Series Data

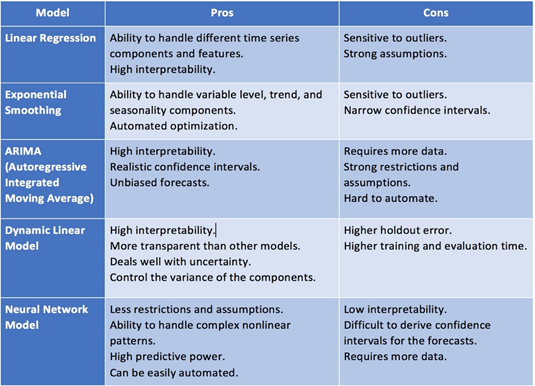

The main objective of a Time Series Analysis is to develop a suitable model to describe the pattern or trend in data with more accuracy. However, forecasting a time series data predicts future outcomes based on the immediate past. Forecasting can be done for closing/opening the rate of stock on daily basis, quarterly revenues of a company, etc., There are various models available in the literature to forecast the time series data. Some of them are:

- Autoregressive Integration Moving Average (ARIMA)

- Simple Moving Average (SMA)

- Exponential Smoothing (SES)

- Neural Network (NN)

- Linear Regression Models

- Logistic Regression

- Support Vector Machine

- Naive Bayes

- Hidden Markov

- VAR

- Gaussian Processes

Well,

many complex models or techniques may be useful in certain cases to forecast a

time series data. They are:

- Neural Networks

Autoregression (NNAR) - RNN

(Recurrent Neural Network) - Bayesian-based models

- Generalized

Autoregressive Conditional Heteroskedasticity (GARCH)

The

performance of the time series models can be interpreted based on its

error terms such as AIC, BIC, Mean Squared Error, etc. and it can be emphasized

for forecasting.

The principle interest for every time series analysis is to split the original series into independent components. The decomposition of time series is much easy to forecast the individual regular patterns produced than from the actual series. Typically, time series are further split into three main components:

- Trend

- Seasonality

- Cycle

Applications

of Time Series Forecasting:

Time

series models usually used to forecast the stock’s performance, interest rate, weather,

etc. In this post, we will look at few situations where time series can be

useful to forecast the future outcome.

Application 1:

In this example, we will look the daily values of the data with time factor available between 2010 and 2016 from Yahoo Finance repository. I extracted the entire time line for 4 related time series (SERIES A values and volumes, SERIES B values and volumes). Forecasting is done for SERIES A values based on the most recent trend (lags) of SERIES A volumes and SERIES B values and volumes. Apart from this, we make use of other dataset from Kaggle to forecast the market sentiment. The data involves top daily news headlines between 2008 and 2016.

Primary step in the time series analysis is

that, one should check whether the time series is approximately stationary and

normalized. For this situation, RNN forecasting is used to predict the outcomes

variable of interest that results in the inference of the future time evolution

of the SERIES A values based on its past trends (including volumes) as well as

the past trend of another SERIES B, and market sentiment.

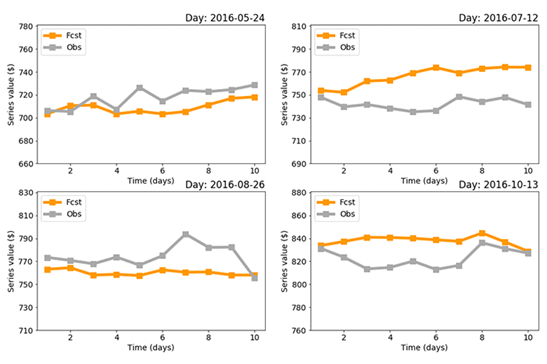

Forecast future values of time series:

It forecasts SERIES A values based on the most recent trend (lags) of SERIES A volumes, SERIES B values and volumes, and market sentiment using ARIMA model. The mean absolute error (MAE) is used to understand the trend in this graph and it is 10, 24, 14, 15 for each sample respectively. The following figure shows a comparison of 10-day forecast.

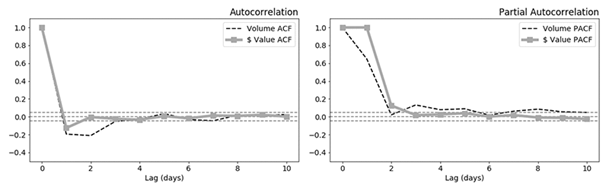

In a traditional regression data, dependent or response variable is influenced by a set of independent variables. The degree of dependence on previous outcomes varies for each case, and can be explained by (ACF) Auto Correlation Factor as given in below figure.

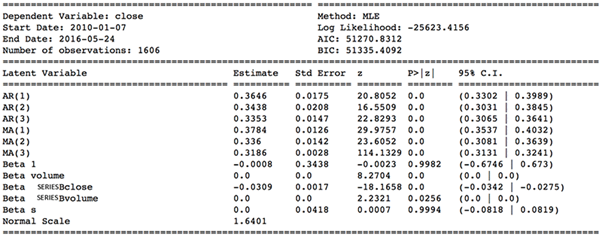

Looking at the ACF and PACF plots, one can choose proper values of the parameters in the model. The results from ARIMA model will look like:

Especially, from the results SERIES B

values significantly influences the forecasting made for SERIES A. The market

sentiment (s) does too but to a lower extent, and volumes are relatively

insignificant for forecasting the SERIES A values with ARIMA.

Speak with our Statswork experts for time series forecasting to build the marketing strategy of financial organisation.

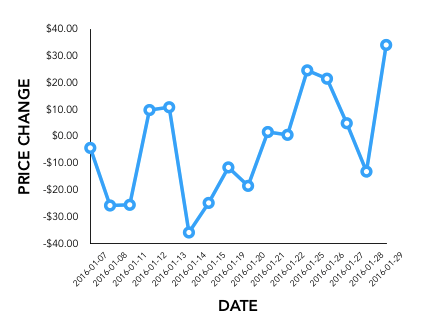

Application 2:

As a second example, we will look at the stock market data from 2016 from Kaggle and analyse the pattern of the data. The data involves stocks of top companies such as Facebook, Apple, Amazon, etc. Here is the trend of daily closing price of stocks for the month of January.

The following graph depicts the trend of price change for a month of January. This is often referred as “momentum” in financial research.

Time series in

financial economics are highly important to analyse the trend or pattern of the

variable of interest using an appropriate model. The above example clearly

depicts the trend in price of the stock and this trend may be helpful in

predicting the future stock values using suitable models as mentioned earlier.

Application 3:

Lastly, let us look at a

situation where the trend of the sales and tractor demand in XYZ manufacturing

company is to be analysed. The company is interested in understanding the

impact of marketing efforts towards the sales. In such situation, finding the

pattern of the sales and demand can be viewed using a well-known ARIMA model

and predict the sales/demand for the upcoming years. In addition, the impact of

the marketing effort can be studied using exogenous variables under ARIMA

model.

To sum up, there are various applications apart from these three are available in our day-to-day life. However, many financial organisation relies on time series forecasting to build their marketing strategy to meet the customer’s needs. Thus, a more proper model should be selected to analyse the pattern of financial data.

References

- Dunning, T., & Friedman, E. (2015). Time Series Databases (1st ed.). California: O’Reilly Media..

- Hyndman, R., & Athanasopoulos, G. (2017). Forecasting: Principles and Practice (2nd ed.)…

- Hyndman, R., & Khandakar, Y. (2008). Automatic time series forecasting: the forecast package for {R}. Journal of Statistical Software, 26(3), 1-22…